If you own or rent your home, you probably pay for a home insurance policy. But, do you really know what is covered and what is excluded? Here are a few tips to help navigate this purchase and alert you to some important options:

Know what is covered. Understand your Policy Declarations page. This explains the important “who,” “what” and “where” of your coverage, as well as the deductible for which you are responsible in the event of a loss. It is also important to know what is NOT covered by the policy – look carefully at the policy exclusions.

Know what part you play in the premium you pay. In Michigan, many carriers use credit-based insurance scores as factors in calculating rates. Be aware of your credit score and fix any errors. Consider a larger deductible to earn a discount. Credits may also be available if you have other coverage, such as your auto insurance, with the same carrier. Frequent claims and poor upkeep of the premises may jeopardize your coverage or significantly increase your cost. Ask your agent about other discounts, such as being a member of a group or having a home alarm system.

Carry adequate limits. In order to include replacement cost on the dwelling, you may be required to insure your home at 100 percent of its replacement cost. Be aware that market value is not the same as replacement cost. Personal property replacement cost (“new for old”) is different than building replacement; you need both, if available. Your liability exposure is extremely important to protect you in the event of a lawsuit, and increasing this coverage is inexpensive. Being a pool owner, a lake resident, or having young drivers in the home are examples of increased exposures. Consider an umbrella or excess liability if your exposure warrants it.

Family dogs can be a problem. With the frequency and severity of dog bite claims, some insurers are very particular about what breeds they will cover. Owning certain types of animals can result in higher premiums or exclusions in coverage. Ask your agent to be sure that your pet is not on an excluded list.

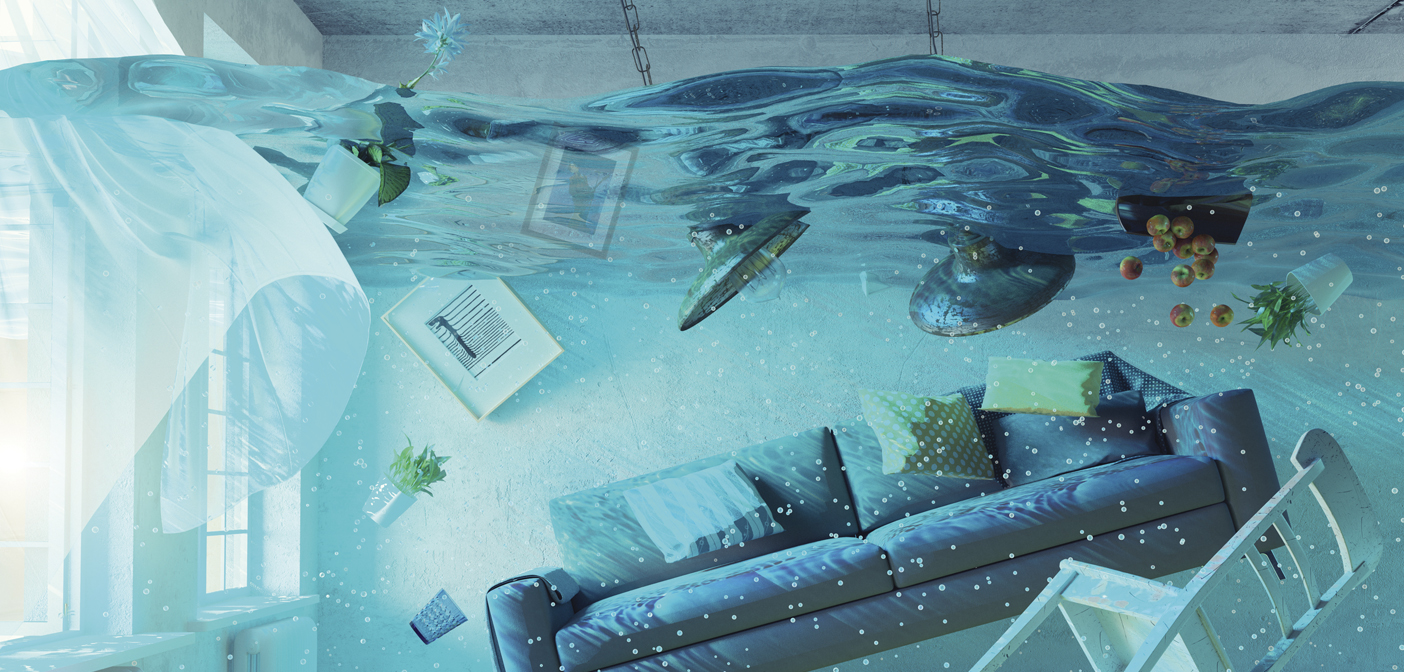

Endorsements may be available for items that are excluded or are limited in the standard policy. Most policies have internal limits for theft of certain items like firearms, jewelry or silver; but you may be able to increase this coverage. Policies also have limitations for water back-up (sewers and drains) and ordinance or law (construction requirements to repair buildings to meet ordinances). In most cases, you can increase these limits. Flood coverage is not included in a homeowner’s policy, but the fact that your lender does not require it doesn’t mean it is not needed. Business exposures or non-owner-occupied dwellings are not intended to be covered by a homeowner’s policy; your agent may be able to provide other solutions. Cyber coverage and identity theft endorsements are important options in today’s technology-driven world – consider purchasing these.

An insurance agent should always be willing to spend time explaining your policy and making sure that you are comfortable with your coverage choices. Asking the right questions enables your agent to develop a package that is right for you.

Provided by Brown & Brown of Michigan